OnMyBubble

Author: AliCatCapital , Last Modified, 2022-03-09 Category: finance Keywords: MEASURING-ALPHA-a-Hedge-Fund-Model-Oscillators

1809 views 45

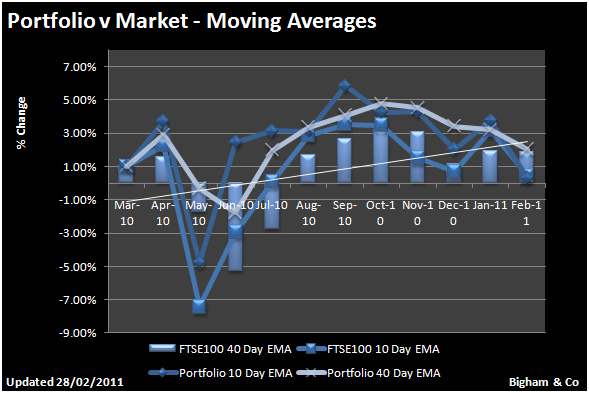

How to measure Alpha when allocating capital to a basket of stocks in a position based trading portfolio.

The use of market oscillation is an effective way to time entering and exiting your positions.The chart above helps us to measure the position of our portfolio relative to the broader market.

In my trading I use this only as a guide, but on an individual stock level, I used the relative position to make trade execution decisions.

This is an incredibly effective way to be disciplined. It is a rule based approach that cannot be overridden by human judgement. The use of these oscillators is therefore a signalling mechanism. Signals in the hedge fund managers models can be based on charts or underlying math built into a Boolean string function, Essentially the market at any point in time can literally be read in English, pre programmed based on the numbers, the chart simply acts a a useful data visualisation of the math.

Of course to rely on the chart and not have an understanding of the intrinsic math is dangerous. The hedge fund managers experience and overall appreciation of the Macro Economic environment is as important as the short term market signal.

This is not about reading charts to understand the market. This is about constructing charts to visualise your math

This approach presupposes that the hedge fund manager has analysed the numbers and determined the rule he or she believes is driving the share price movement, then building a model with charts to better visualise the math.It is quantitative modelling as apposed to Chartism or Technical Analysis. But there are merits and risks in both of course, but it worth mentioning the distinction.

Keywords:MEASURING-ALPHA-a-Hedge-Fund-Model-Oscillators

Blog title: MEASURING ALPHA a Hedge Fund Model Oscillators( 29 articles!)

Trading with OMBCoin a digital currency for the new millenium

Understanding Big debt Crisis By Ray Dalio

My Top Ten Tips For Budding Online traders Million Dollar Trading

Million Dollar Trading DISCOVER HOW I BEAT THE MARKET CONSISTENTLY

DISCOVER HOW I BEAT THE MARKET CONSISTENTLY Is it easy to trade stocks online for a living

Is it easy to trade stocks online for a living Trade Back Testing

Trade Back Testing  Theresa May Strikes Deal on EU Withdrawal Agreement

Theresa May Strikes Deal on EU Withdrawal Agreement European Medicine Agency

European Medicine Agency Excel Trading System Development

Excel Trading System Development Excel Trading System

Excel Trading System  Trading System Risk Analytics

Trading System Risk Analytics How do online traders manage risk?

How do online traders manage risk? What is the Investment Outlook for 2018?

What is the Investment Outlook for 2018? MEASURING ALPHA a Hedge Fund use of Oscillators

MEASURING ALPHA a Hedge Fund use of Oscillators Excel Trading System

Excel Trading System  Deal Statement Template

Deal Statement Template Excel Trading System

Excel Trading System  MEASURING ALPHA a Hedge Fund Frequency Distribution of Returns

MEASURING ALPHA a Hedge Fund Frequency Distribution of Returns online trading in 2017

online trading in 2017 What is the Investment Outlook for 2020?

What is the Investment Outlook for 2020? MEASURING ALPHA a Hedge Fund Model Prices

MEASURING ALPHA a Hedge Fund Model Prices About AliCat Capital Management

About AliCat Capital Management MEASURING ALPHA a Hedge Fund Model

MEASURING ALPHA a Hedge Fund Model Performance Brief for AliCat Capital

Performance Brief for AliCat Capital Generating 44% ROE from £ 50M

Generating 44% ROE from £ 50M How To Get Rich The Felix Dennis Way

How To Get Rich The Felix Dennis Way online trading in 2017

online trading in 2017 online trading systems

online trading systems music (58)

music (58) fashion (16)

fashion (16) car (10)

car (10) real_estate (27)

real_estate (27) beauty (9)

beauty (9) travel (22)

travel (22) design (31)

design (31) food (44)

food (44) dating (8)

dating (8) movie (13)

movie (13) photography (5)

photography (5) law (6)

law (6) health (17)

health (17) green (4)

green (4) technology (16)

technology (16) SEO (5)

SEO (5) marketing (11)

marketing (11) history (10)

history (10) lifestyle (17)

lifestyle (17) university (3)

university (3) dog (1)

dog (1) money (10)

money (10) business (59)

business (59) fitness (12)

fitness (12) wedding (8)

wedding (8) education (3)

education (3) science (1)

science (1) shopping (7)

shopping (7) entertainment (11)

entertainment (11) sports (17)

sports (17) cat (6)

cat (6) social_media (1)

social_media (1) medical (3)

medical (3) wine (4)

wine (4) celebrity_gossip (4)

celebrity_gossip (4) DIY (5)

DIY (5) nature (2)

nature (2) gaming (65)

gaming (65) pet (6)

pet (6) finance (35)

finance (35) political (4)

political (4) career (8)

career (8) parenting (4)

parenting (4) economics (17)

economics (17)advertisement

MEASURING-ALPHA-a-Hedge-Fund-Model-Oscillators OnMyBubble.com